Quick Facts

- 2026 QLAC Limit: The maximum allowable contribution has increased to $210,000 per person, allowing for greater sheltering of retirement assets.

- Housing Wealth: US seniors over age 62 currently hold a record $14.6 trillion in untapped home equity as of the third quarter of 2025.

- Social Security Risk: Emerging projections suggest a potential 23% benefit cut by 2033, making alternative home equity retirement income a necessity rather than a luxury.

- The Hybrid Strategy: Integrating a Home Equity Conversion Mortgage with a Qualified Longevity Annuity Contract can significantly increase liquid savings over a long retirement horizon.

- Tax-Free Efficiency: Properly structured home equity retirement income provides tax-free cash flow through a line of credit, helping retirees preserve their portfolios during market volatility.

- Asset Depletion: High-net-worth individuals can use asset depletion models to qualify for reverse mortgages even without high traditional monthly income.

As homeowners aged 62+ hold a record $14.66 trillion in housing wealth, unlocking home equity retirement income has become a vital pillar for a secure future. This guide explores the sophisticated HECM and QLAC strategy, designed to bridge the Social Security gap and provide longevity insurance for the mass affluent. By leveraging illiquid assets, retirees can manage sequence of returns risk and maintain cash flow without selling their primary residence, while also creating a financial buffer for unplanned health or long-term care expenses.

The Social Security Gap and the 2026 Mass Affluent Strategy

Modern retirement planning for the mass affluent cohort—those with liquid assets between $500,000 and $5 million—requires more than just a diversified stock portfolio. As we look toward the 2026 fiscal environment, the primary challenge is not just wealth accumulation, but sustainable distribution. Many in this demographic are "house-rich and cash-constrained," sitting on significant property value while their investment accounts remain vulnerable to market swings.

The magnitude of this opportunity is staggering. Data from the National Reverse Mortgage Lenders Association indicates that senior housing wealth reached a record $14.66 trillion in late 2025. For the typical retiree, this equity represents a dormant engine that can be ignited to combat the rising cost of living and potential shifts in Social Security stability.

A critical component of this strategy is managing sequence of returns risk. This is the danger that a market downturn early in retirement will force a retiree to sell equities at a loss to cover living expenses, permanently impairing the portfolio’s longevity. By using home equity retirement income as a flexible buffer, retirees can draw from their home instead of their stocks during a bear market. Vanguard research estimates that extracting the full value of home equity could increase retirement readiness by 20 percentage points for many baby boomers. This ensures that roughly 60% of retirees can stay on track to maintain their lifestyle even through economic turbulence.

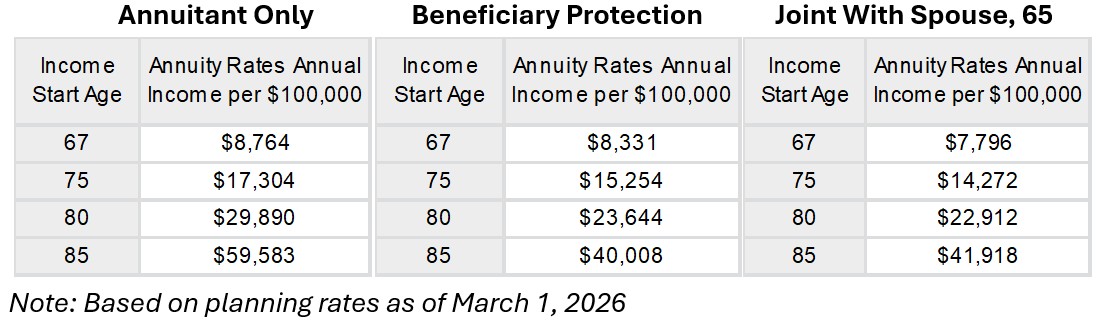

Deep Dive: 2026 QLAC Rules and RMD Mitigation

For many investors, the Required Minimum Distribution is a tax burden that forces them to withdraw money they don't necessarily need, pushing them into higher tax brackets. The SECURE Act 2.0 introduced pivotal changes to the Qualified Longevity Annuity Contract, or QLAC, which have been further refined for the 2026 tax year.

Under the current rules, an individual can move up to $210,000 from their traditional IRA or 401(k) into a QLAC. The primary appeal of this move lies in the deferred income annuity tax benefits. The funds used to purchase the QLAC are removed from the math used to calculate your RMDs. This allows the remaining balance in your retirement accounts to grow tax-deferred for longer, significantly reducing your annual tax liability during your 70s and early 80s.

Key features of the QLAC include:

- Tax Deferral: Payouts can be delayed until as late as age 85, allowing the principal to grow without immediate tax erosion.

- Longevity Insurance: It provides a guaranteed check for life, regardless of how long you live or how the stock market performs.

- Inflation Protection: Many contracts offer cost-of-living adjustments to ensure purchasing power is maintained decades into the future.

When you weigh the tax advantages of deferred income annuities against a standard withdrawal strategy, the math often favors the QLAC for those concerned about "outliving their money." By the time the payments trigger at age 85, they act as a permanent floor of income that supports advanced healthcare needs or assisted living costs.

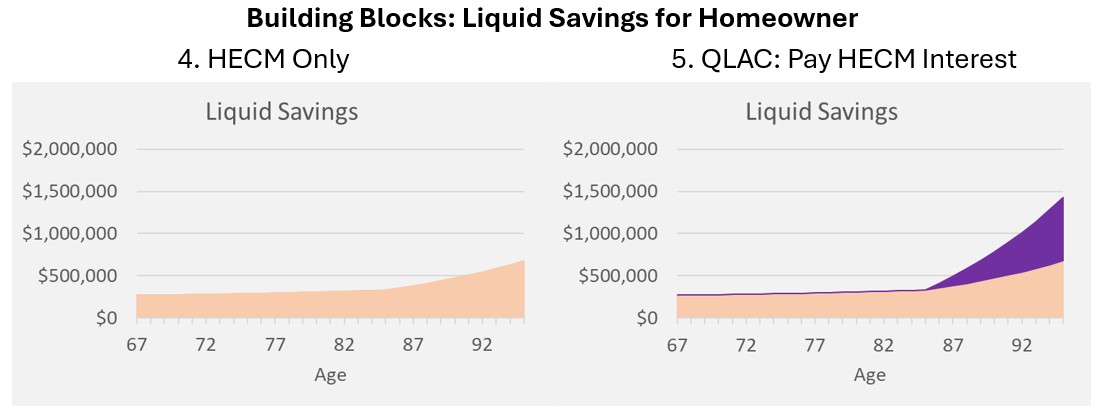

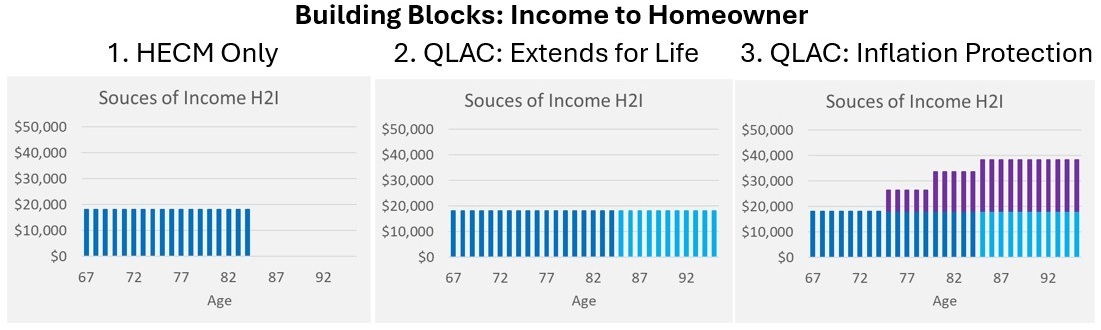

The HECM-QLAC Power Move: Bridging the Age 85 Gap

The most sophisticated way to deploy these tools is through a HECM and QLAC combination strategy, often referred to as a Home-to-Income or H2I model. This two-phase approach addresses the two different halves of a standard retirement.

In Phase One (Ages 62–84), the homeowner secures a Home Equity Conversion Mortgage (HECM). Rather than taking a lump sum, they establish a HECM line of credit. The beauty of this credit line is that it grows over time at the same interest rate charged on the loan balance. It provides a source of non-taxable cash that can be used to supplement lifestyle needs or pay for home repairs without touching the investment portfolio.

In Phase Two (Age 85+), the QLAC triggers. The guaranteed lifetime payments begin just as the retiree enters their mid-80s—a period where medical expenses often spike. This transition from housing wealth monetization to annuity income ensures a seamless cash flow profile.

One of the most innovative aspects of this HECM and QLAC strategy is how the two products interact for tax purposes. If the income from the QLAC is used to pay down the interest on the HECM, the retiree may be able to claim a tax deduction for that interest payment. This can effectively offset the taxable income generated by the annuity, creating a highly efficient financial loop. Using this reverse mortgage for retirement income guide correctly means you aren't just spending your assets; you are optimizing the timing of how they are taxed and spent.

Qualification Mechanics: Asset Depletion & Residency Rules

While many believe reverse mortgages are only for those with low income, the modern reality is quite the opposite. To qualify for a HECM, lenders use a technique called Asset Depletion. This allows affluent homeowners to use their brokerage accounts and retirement funds to "qualify" for the loan, even if they don't have a traditional salary.

The underwriting process often includes a "125% gross up" for non-taxable income sources, such as Social Security. This math ensures that the homeowner has enough residual income to cover property taxes, insurance, and maintenance. However, there are strict rules to maintain the loan in good standing:

- The 12-Month Rule: If a homeowner resides in a healthcare facility or nursing home for more than 12 consecutive months, the HECM may become due and payable. This makes the longevity insurance provided by the QLAC even more important, as it can help fund in-home care to avoid triggering this rule.

- Maintenance Requirements: You must keep the home in reasonable repair and continue paying all property-related expenses.

- Capped Fees: The Federal Housing Administration (FHA) caps the origination fees on HECMs at $6,000, ensuring that the costs of setting up this plan remain transparent and regulated.

By understanding these mechanics, homeowners can turn their property into a dynamic financial tool while ensuring they meet the residency and financial requirements to protect their estate legacy.

Decision Matrix: HECM vs. Traditional Home Equity Loans

Choosing the best ways to access home equity depends heavily on your current cash flow and long-term goals. Traditional Home Equity Lines of Credit (HELOCs) are often easier to set up but carry risks that a HECM does not. For instance, HELOCs usually have a 10-year draw period followed by a repayment period, and banks can freeze the line of credit if home values drop.

| Feature | HECM (Reverse Mortgage) | HELOC (Traditional) | QLAC (Annuity) |

|---|---|---|---|

| Monthly Payment Required | No | Yes | N/A (Receives Payment) |

| Income Qualification | Asset Depletion / Residual | DTI Cap (43-50%) | Initial Principal Only |

| Tax Impact | Tax-Free Proceeds | Tax-Deductible (Specifics) | Tax-Deferred Growth |

| Growth of Credit Line | Yes, guaranteed growth | No | N/A |

| Primary Goal | Cash flow & longevity | Short-term liquidity | Income floor at age 85 |

Grace’s Tip: If your goal is to eliminate monthly expenses and maximize your credit line over 20 years, the HECM is superior. If you just need $50,000 for a kitchen remodel and plan to pay it back within 24 months, a traditional HELOC remains the better choice.

FAQ

How can I use home equity to supplement my retirement income?

There are several methods, but the most common for long-term planning include a HECM line of credit, which allows you to draw funds as needed, or a HECM term option that provides a fixed monthly payment. These options allow you to stay in your home while converting property value into usable cash.

Is retirement income from home equity taxable?

Generally, no. Funds received from a reverse mortgage or home equity loan are considered loan proceeds, not earned income, and are therefore not subject to federal income tax. This makes them an excellent tool for managing your tax bracket in retirement.

What is the difference between a home equity loan and a reverse mortgage?

A traditional home equity loan requires you to make monthly principal and interest payments immediately. A reverse mortgage (HECM) does not require monthly payments for as long as you live in the home, although you remain responsible for taxes and insurance.

What are the best ways to access home equity during retirement?

The best way depends on your timeline. For immediate cash needs, a HELOC is common. For those looking for lifetime security and a growing safety net, a HECM is typically the preferred vehicle. High-net-worth individuals often use a HECM in tandem with other investment engines.

Are there risks to using home equity as a source of income?

Yes, the primary risks include the eventual depletion of home equity for heirs and the requirement to move out if the home can no longer be maintained. Additionally, if the owner spends more than 12 months in a medical facility, the loan may become due.

Final success in setting up a home equity retirement income plan depends on coordination between your mortgage specialist and your financial advisor. Ensuring that your HECM acts as a liquidity bridge while your QLAC provides an income floor allows you to navigate the complexities of modern retirement with confidence. Always consult with a professional who provides fiduciary financial advice to ensure these strategies align with your specific estate goals and tax situation.