Quick Facts

- 2025 Reinvestment Hard Deadline: September 11, 2026, for many capital gains reported via Schedule K-1.

- Tax Efficiency: Utilizing these funds can result in a potential 23.36% increase in after-tax cash compared to paying taxes immediately.

- Asset Flexibility: Reinvest only the gain portion and keep your principal, unlike other transition strategies that require full reinvestment.

- Rural Incentive: Newer provisions offer a 30% basis step-up for Qualified Rural Opportunity Funds, significantly higher than previous incentives.

- Compliance: Mandatory filing of Form 8996 and Form 8997 is required to avoid new penalties that can reach $500 per day.

- Amended Returns: Investors can still elect to defer 2025 gains even after they have filed their initial tax return for the year.

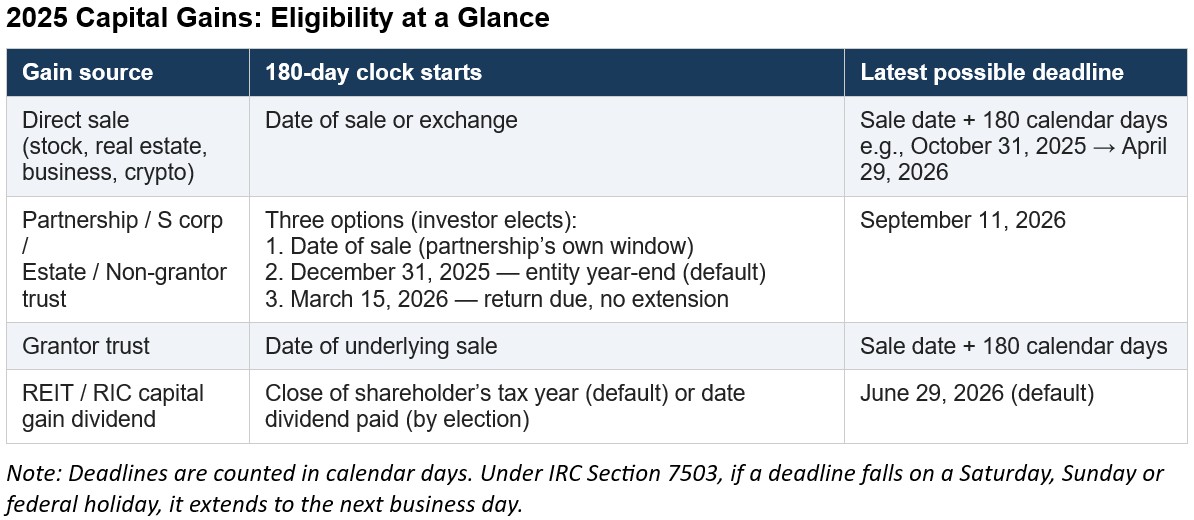

The deadline to reinvest 2025 capital gains into Qualified Opportunity Funds depends on the asset type and realization date. For direct sales of real estate, the capital gains tax deferral 180-day window begins on the closing date. For gains reported via partnerships or S corporations, the window typically begins on December 31, 2025, or the entity's tax filing due date of March 15, 2026, meaning some investors have until September 2026 to complete a QOF investment.

The deadline to reinvest 2025 capital gains into Qualified Opportunity Funds depends on your asset type. For real estate sold directly, the clock is ticking, but for partnership gains reported via Schedule K-1, you may have until September 2026. This guide explores the Qualified Opportunity Funds 180-day window calculation and how to amend your tax return to capture deep tax savings before the 2026 mandatory recognition date. By the end of 2023, Qualified Opportunity Funds raised an estimated total of $112 billion to $150 billion in equity since the program's inception in 2018.

The 180-Day Window: Critical Deadlines for 2025 Gains

Precision regarding the Internal Revenue Service deadlines is the difference between a successful tax deferral and a massive tax bill. The clock does not start at the same time for everyone. Understanding how to handle your specific asset realization is the first step in qualified opportunity fund 180 day window calculation.

For an individual selling a property directly, the window is straightforward: it starts on the date of the sale. However, for those receiving gains through a partnership, S corporation, or a trust, there are three distinct choices for when the window begins. This flexibility often allows investors to wait until well into the next year to make their investment decision.

- Individual Direct Sales: The window begins on the date the asset was sold. If you sold a rental property on July 1, 2025, your window closes in late December 2025.

- Entity Year-End: For gains from a partnership or S corporation, investors can choose to start their window on December 31, 2025. This provides a deadline of late June 2026.

- Entity Filing Deadline: Investors can also choose the entity’s tax return due date (excluding extensions). This is typically March 15, 2026. Starting the clock here extends the opportunity to reinvest until September 11, 2026.

This extended timeline is why the partnership capital gain QOF deadline June 2026 is such a critical milestone for many sophisticated investors. If you missed the window for a direct sale, check if any of your gains were actually Section 1231 Gains coming through a business entity, as these may still be eligible for reinvestment today.

Amending Your Return: It's Not Too Late for QOF

One of the most common questions from investors is: can I still invest 2025 gains into QOF in 2026? Unlike a 1031 exchange, which requires naming a replacement property within 45 days and closing within 180, Qualified Opportunity Funds are much more forgiving after the fact.

You can still invest in a fund after you have already filed your tax return for the year the gain was realized. If you realized a gain in 2025 and already paid the tax on your return filed in April 2026, you haven't necessarily lost the opportunity. As long as you are still within the 180-day window (which, as noted above, can extend to September 2026 for K-1 gains), you can perform what is known as "curing" the gain.

The process involves filing an amended tax return to elect QOF deferral treatment. By submitting an amended return along with Form 8949 and Form 8997, you effectively move the capital gain out of the original tax year. This allows you to claim a refund for the capital gains tax you previously paid.

When you amend your return, you must ensure that your Adjusted Basis is tracked correctly. The Internal Revenue Service requires rigorous reporting of these deferred gains to ensure they are captured by the mandatory deadline of December 31, 2026.

QOF vs. 1031 Exchange for Real Estate Investors

Real estate investors often default to the 1031 exchange, but for many, reinvesting real estate capital gains into opportunity funds offers more flexibility and better long-term outcomes. The primary difference lies in what you must reinvest. A 1031 exchange requires you to reinvest the entire sale proceeds into a new property to avoid tax. In contrast, Qualified Opportunity Funds only require you to reinvest the capital gain portion.

| Feature | 1031 Exchange | Qualified Opportunity Fund |

|---|---|---|

| Amount to Reinvest | Full Sales Proceeds | Capital Gains Only |

| Timeline to Identify | 45 Days | Not Applicable |

| Asset Types | Real Estate Only | Real Estate, Stocks, Business Assets |

| Tax on New Growth | Deferred (until next sale) | 100% Tax-Free (after 10 years) |

| Depreciation Recapture | Deferred | Generally recognized in 2026 |

Because you can keep your original principal, QOFs provide immediate liquidity that a 1031 exchange cannot. Furthermore, the tax-free growth benefit is unparalleled. If you hold your QOF investment for at least 10 years, any appreciation on that new investment is exempt from federal capital gains tax and the Net Investment Income Tax. This creates a massive compounding advantage for the investor.

Advanced 2026-2027 Strategies: Rural Funds and Bridge Investing

The landscape of Opportunity Zones is evolving with new legislative updates. A QOF bridge strategy allows investors to defer 2025 gains today while positioning for future legislative updates like Opportunity Zone 2.0. By reinvesting into a QOF now, investors can later sell that interest to trigger a fresh 180-day window. This allows for the potential reinvestment of capital into new funds starting in 2027 to capture enhanced tax incentives provided by updated regulations.

Sophisticated accredited investors are also looking closely at the OBBBA 2025 provisions, which introduce the concept of a Rural Opportunity Fund. Traditional Opportunity Zones offered a 10% or 15% basis step-up if held for certain periods. Under the new rural incentives, investors may see a 30% basis step-up. This significantly reduces the amount of the original 2025 gain that is eventually taxed in 2026.

This bridge strategy is particularly useful for those in a high marginal income bracket who expect significant appreciation. By locking in the deferral now, you bypass the immediate tax hit and keep that money working in the market, effectively using the government's tax money as an interest-free loan until the 2026 recognition date.

Compliance and Reporting under OBBBA 2025

As the program matures, the Internal Revenue Service has increased its focus on compliance. New regulations introduced in mid-2025 have significantly raised the stakes for those who fail to report their holdings correctly.

OBBBA 2025 Penalty Alert: Starting July 2025, the failure to file accurate information reports regarding Opportunity Zone investments can result in penalties of $500 per day. This makes the accurate filing of Form 8997 essential for every investor.

If you are reinvesting gains, you must manage two primary compliance streams:

- Fund Level: The fund must file Form 8996 annually to certify that it maintains at least 90% of its assets in Qualified Opportunity Zone property.

- Investor Level: You must file Form 8997 every year with your tax return to track the amount of deferred gains and your adjusted basis in the fund.

It is also important to remember the mandatory tax recognition date. Under the original rules, all capital gains reinvested into these funds must be recognized and taxed by December 31, 2026. While the tax on the growth of the fund is eliminated after 10 years, the tax on the original 2025 gain is only deferred until that 2026 deadline. You must plan for that liquidity event well in advance.

FAQ

How do the tax benefits of a QOF work?

There are three main benefits: deferral of tax on the original gain until 2026, a potential step-up in basis that reduces the original gain by up to 30%, and complete tax-free growth on the new investment if held for at least 10 years.

What types of capital gains are eligible for a QOF?

Almost any capital gain is eligible, including those from the sale of stocks, bonds, precious metals, and real estate. This includes Section 1231 Gains and capital gains from the sale of a business, though depreciation recapture is generally taxed differently.

Is there a deadline for investing in a Qualified Opportunity Fund?

Yes, investors generally have a 180-day window to reinvest their gains. The specific start date of this window depends on whether the gain was realized by an individual, a partnership, or an S corporation.

How is a QOF different from a 1031 exchange?

A QOF only requires the reinvestment of the taxable gain, whereas a 1031 exchange requires the reinvestment of the entire sale proceeds. Additionally, QOFs allow for tax-free appreciation after 10 years, while a 1031 exchange only continues to defer taxes.

What happens to a QOF investment after 10 years?

After a 10-year holding period, the investor can elect to increase the basis of their QOF investment to its fair market value on the date of sale. This effectively makes all appreciation on the QOF investment entirely free from federal capital gains tax.

The window for 2025 gains is closing, particularly for direct real estate sales. However, if you are a partner in a real estate syndicate or an S corporation shareholder, you likely have until the partnership capital gain QOF deadline June 2026 or even September 2026 to act. Given the complexity of the new reporting requirements and the significant potential for a 23.36% after-tax boost, consulting with a tax professional today is essential to ensure you don't miss these high-value deadlines.