Quick Facts

- 2026 TFSA Limit: The annual contribution room is $7,000.

- 2026 RRSP Limit: You can contribute 18% of your previous year’s earned income, up to a maximum of $33,810.

- Income Threshold: $55,867 is the critical federal pivot point for determining tax efficiency between accounts.

- Home Buyer Benefit: The Home Buyers’ Plan (HBP) allows a withdrawal limit of $60,000 from your RRSP.

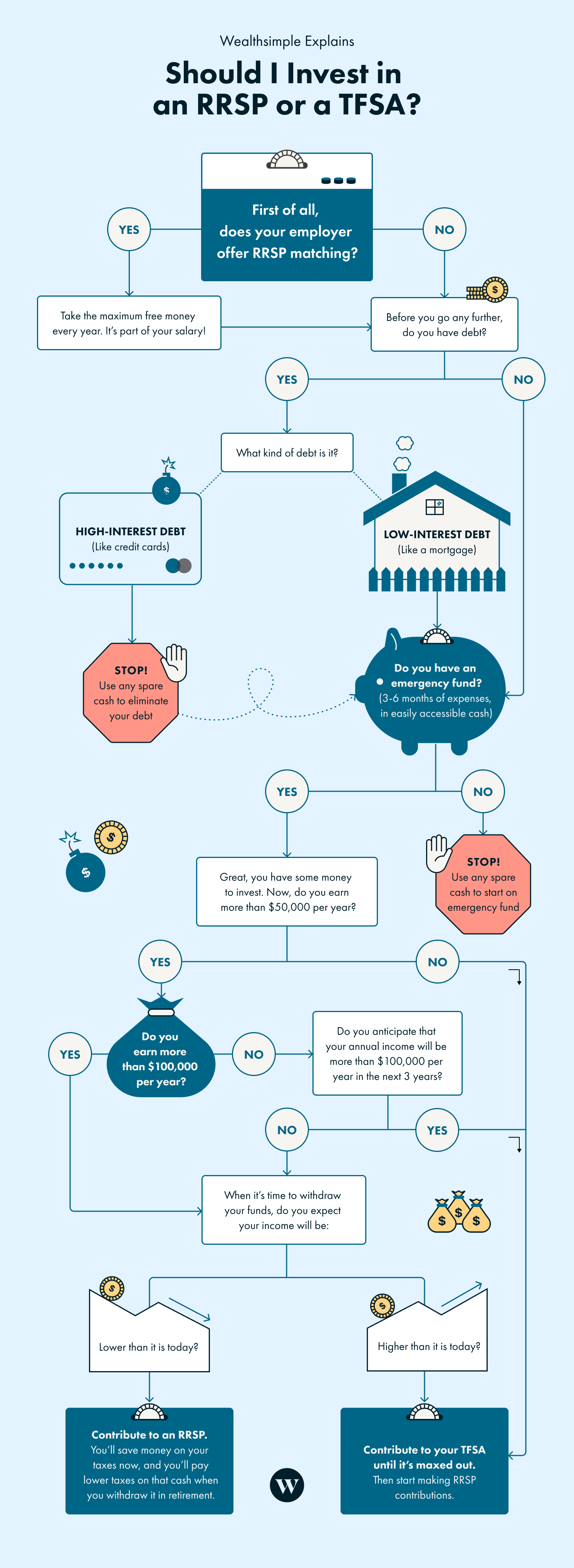

- The Match Rule: Always prioritize employer RRSP matches to capture immediate 100% returns.

- Withdrawal Flexibility: TFSA withdrawals are tax-free and the room is restored the following year, while RRSP withdrawals are taxed as income.

The choice between an RRSP and a TFSA is primarily driven by your annual income and tax bracket. In 2026, if you earn more than $55,867, RRSP contributions are often prioritized to lower your taxable income. However, for many, the TFSA offers better flexibility. This guide helps you navigate the RRSP vs TFSA debate to save money faster. To optimize your personal finance strategy in 2026, prioritize an RRSP if you are in a high tax bracket to lower taxable income, or a TFSA if you need tax-free growth and withdrawal flexibility for short-to-mid-term goals.

Understanding the Basics: Rules and Limits in 2026

When planning your financial future, it is essential to distinguish between tax-deferred and tax-free growth. A Registered Retirement Savings Plan (RRSP) is tax-deferred, meaning you get a tax break now but pay taxes when you take the money out. Conversely, a Tax-Free Savings Account (TFSA) uses after-tax income; you do not get a deduction today, but you will never pay a cent of tax on the investment growth or the withdrawals.

For the 2023 tax year, Statistics Canada noted that the median contribution for tax filers who only used a Tax-Free Savings Account (TFSA) was $6,500, illustrating how many Canadians prioritize the annual limit. In 2026, that annual limit is $7,000. If you have been eligible since 2009 and have never contributed, your cumulative TFSA room could be as high as $109,000.

The RRSP functions differently. Your contribution room is capped at 18% of your earned income from the previous year, up to a maximum of $33,810 for 2026. This makes the RRSP a powerful tool for high earners but requires more careful tracking of your Notice of Assessment from the Canada Revenue Agency.

Understanding TFSA vs RRSP withdrawal rules is just as vital as knowing the limits. If you pull money out of a TFSA, that contribution room is added back to your total on January 1st of the following year. RRSP withdrawals, however, result in a permanent loss of that contribution room, unless you are using specific programs like the Home Buyers' Plan.

The $55,867 Rule: Choosing Based on Your Income

The most significant factor in the RRSP vs TFSA decision is your marginal tax rate. This is the amount of tax you pay on your next dollar of income. In 2026, the federal tax bracket shifts at $55,867. If your income is below this threshold, your immediate tax savings from an RRSP contribution are relatively small.

Consider the math: for a Canadian earning over $250,000 at a 50% marginal tax rate, a $10,000 contribution to an RRSP provides an immediate $5,000 tax reduction. In contrast, an individual earning less than $55,000 at a 15% rate would see only a $1,500 reduction for the same contribution.

For lower-income earners, prioritizing RRSP vs TFSA for income under 55000 usually leans toward the TFSA. Not only is the tax deduction less impactful now, but RRSP withdrawals in retirement count as net income. This can trigger "clawbacks" on federal benefits. The impact of RRSP withdrawals on OAS and GIS can be severe, potentially reducing the GIS payments that lower-income seniors rely on. Since TFSA withdrawals are not considered income, they have zero impact on these benefits, making the TFSA a more protective vehicle for those in lower tax brackets.

For RRSP vs TFSA for high income earners 2026, the strategy flips. If you are in your peak earning years, the goal is to take the deduction now at a high rate (e.g., 45-50%) and withdraw the funds in retirement when you are likely in a lower bracket. This "tax arbitrage" is the primary engine of RRSP wealth creation.

The Strategic Hierarchy: FHSA vs Employer Match vs TFSA

In 2026, savvy investors do not just choose one account; they follow a hierarchy of needs to ensure no "free money" is left on the table. Your personal finance strategy should look like a funnel, where money flows into the most efficient buckets first.

- Employer RRSP Match: If your company offers a 5% match, that is a guaranteed 100% return on your investment. Prioritizing employer RRSP match vs TFSA is a no-brainer.

- First Home Savings Account (FHSA): If you intend to buy a home, the FHSA is the gold standard. It combines the tax-deductibility of an RRSP with the tax-free withdrawals of a TFSA. Even if you don't buy a home, you can eventually roll this into an RRSP.

- TFSA or RRSP: Based on the $55,867 income rule mentioned above.

| Feature | TFSA | RRSP | FHSA |

|---|---|---|---|

| Tax on Contribution | After-tax (No deduction) | Pre-tax (Deduction) | Pre-tax (Deduction) |

| Growth | Tax-free | Tax-deferred | Tax-free |

| Withdrawal Tax | $0 | Taxed as income | $0 (for home) |

| 2026 Limit | $7,000 | $33,810 max | $8,000 |

| Goal | Flexibility/Retirement | Long-term Retirement | First Home |

If your goal is buying a home, the RRSP and TFSA tax advantages still play a role. The RRSP Home Buyers’ Plan (HBP) now allows you to withdraw up to $60,000 tax-free, but it must be paid back within 15 years. The TFSA requires no payback, making it a "stress-free" down payment bucket.

Advanced Moves: Reinvesting the Tax Refund

The true power of an RRSP is often lost because people spend their tax refunds on consumer goods. To level the playing field in the RRSP vs TFSA comparison, you must use the refund to fuel further growth. This is known as a blended strategy or reinvesting RRSP tax refund into a TFSA strategy.

Imagine you earn $120,000 and contribute $10,000 to your RRSP. Depending on your province, you might receive a tax refund of approximately $4,000. If you take that $4,000 and immediately deposit it into your TFSA, you are effectively using the government’s money to build tax-free wealth. This creates a powerful engine for compound interest.

Research shows that Canadians are increasingly favoring this flexible approach. Statistics Canada found that average Canadian household contribution to TFSAs grew by 75.0% between 2009 and 2020, which significantly outpaced the 21.1% growth seen in RRSP contributions. This shift suggests that the versatility of the TFSA is becoming the preferred tool for modern wealth accumulation.

Common Mistakes and CRA Penalties

As a tax editor, I often see well-intentioned savers lose their gains to avoidable penalties. The Canada Revenue Agency is strict about contribution limits. If you over-contribute to either account, you will face a penalty of 1% per month on the excess amount.

One common trap involves TFSA vs RRSP withdrawal rules. For a TFSA, if you withdraw $5,000 in July, you cannot put that $5,000 back in until January 1st of the next year (unless you have other unused room). Doing so mid-year counts as a new contribution and often triggers that 1% penalty.

For the RRSP, early withdrawals (those not for the HBP or Lifelong Learning Plan) are subject to an immediate withholding tax. The bank will often take 10% for withdrawals up to $5,000, 20% for amounts up to $15,000, and 30% for anything over $15,000. Crucially, this is just a pre-payment; if your total income is high, you may owe even more when you file your taxes in April.

FAQ

Is it better to put money in an RRSP or a TFSA?

The answer depends on your income. If you earn more than $55,867, an RRSP is usually better for the immediate tax deduction. If you earn less, or if you need the money before retirement, the TFSA is superior because withdrawals are tax-free and more flexible.

Should I prioritize my RRSP or TFSA if I have a low income?

For those with a low income, the TFSA should be the priority. The tax savings from an RRSP are minimal at lower brackets, and RRSP withdrawals could reduce your eligibility for future federal benefits like the Guaranteed Income Supplement.

Does an RRSP contribution reduce my taxes?

Yes. An RRSP contribution is deducted from your gross income. For example, if you earn $80,000 and contribute $10,000 to an RRSP, the government taxes you as if you only earned $70,000, usually resulting in a tax refund.

Can I use an RRSP or TFSA for a home down payment?

Yes. You can use the RRSP Home Buyers’ Plan to withdraw up to $60,000, which must be repaid. A TFSA can also be used; it has no withdrawal limit (other than your balance) and does not need to be repaid, though it lacks the initial tax deduction of the RRSP.

Can I hold both an RRSP and a TFSA at the same time?

Absolutely. In fact, most financial planners recommend using both. You can use the RRSP for long-term retirement security and the TFSA for short-term goals, emergency funds, or as a place to reinvest your RRSP tax refunds.

To make the best choice for your 2026 finances, calculate your specific tax bracket and review your unused contribution room on the CRA My Account portal before the March 2, 2026 RRSP deadline. Planning ahead ensures you keep more of your hard-earned money and grow it faster.