Quick Facts

- 2026 401k Limit: The individual contribution limit rises to $24,500, offering more room for tax-deferred growth.

- Employer Match ROI: Capturing your full employer match provides an immediate 100% return, making it the highest priority in any retirement savings hierarchy.

- HSA Priority: Once the match is met, the triple tax advantage of a Health Savings Account makes it a superior vehicle for long-term wealth.

- High-Interest Debt: Financial experts suggest clearing high-interest credit card debt before contributing a single dollar beyond your employer match.

- Super Catch-up: Participants aged 60-63 can contribute up to $11,250 extra in 2026, a significant boost for those near retirement.

- Roth Mandate: High earners with prior-year FICA wages above $150,000 must now designate catch-up contributions as Roth, impacting tax planning for 2026.

Deciding your 401k contribution strategy for 2026 requires looking beyond the employer match. While the employer match is a vital foundation that creates an immediate return on your investment, your next dollar might work harder in an HSA or a Roth IRA depending on your tax bracket and liquidity needs.

The Sequential Guide: Should You Save More Than the Match?

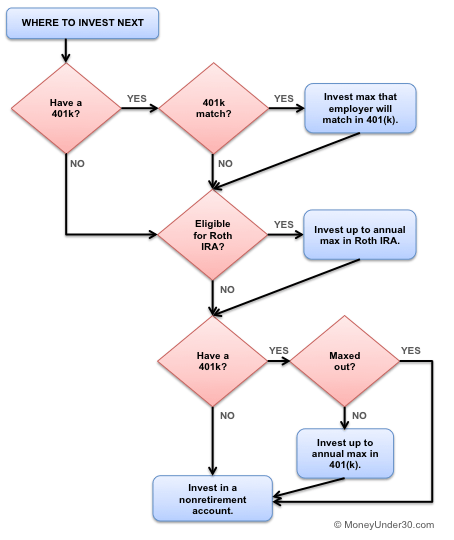

For many investors, the employer match feels like the natural finish line for retirement planning. If your company matches up to 6% of your salary, you contribute 6%, and the task is marked as complete. However, when we look at the broader retirement savings hierarchy, the match is actually the starting line, not the goal. Whether or not you should save more than the employer match depends on where you stand in your financial journey.

While the match provides an unbeatable return, the total amount saved often falls short of the 12% to 15% of annual salary that institutions like Vanguard and Fidelity typically recommend for a comfortable retirement. In early 2024, Fidelity reported that the total average 401k savings rate reached a record 14.3%, which was composed of a 9.5% employee contribution and a 4.8% employer match. This data suggests that successful investors are already recognizing that investing beyond 401k match levels is necessary to maintain their lifestyle in the future.

The question of how much to contribute to 401k after employer match mandates is less about the total dollar amount and more about the sequence of accounts. By following a structured 401k contribution strategy, you can maximize your tax efficiency and ensure your money is working as hard as possible.

Step 1: Secure the Match and Clear Debt

The first rule of investment fundamentals is never to leave free money on the table. A 401k match is a guaranteed windfall. If your employer offers a dollar-for-dollar match, that is an immediate 100% return. No stock, bond, or real estate investment can reliably compete with that. Consequently, the first step of any retirement savings hierarchy is contributing exactly enough to trigger that full match.

However, once that match is secured, the next logical move isn't always to keep pouring money into the 401k. This is where 401k contribution order with high interest debt becomes a critical calculation. If you are carrying credit card balances with interest rates ranging from 20% to 30%, that debt is effectively a "reverse investment" that erodes your net worth faster than a 401k can build it.

Before you consider is it worth contributing to 401k beyond match levels, you must address two non-negotiable financial pillars:

- High-Interest Debt Payoff: Any debt with an interest rate higher than 7% or 8% should generally be eliminated before making additional voluntary 401k contributions.

- Emergency Fund Liquidity: Ensure you have three to six months of living expenses in a high-yield savings account. Retirement accounts are often difficult or expensive to access in a pinch; liquidity ensures you don't have to raid your 401k when life throws a curveball.

Step 2: The Strategic Pivot—HSA and Roth IRA

Once the match is captured and high-interest debt is gone, it is often time to hit the "pause" button on your 401k. This is where many investors miss out on significant tax advantages. Instead of continuing with the 401k, the 401k vs roth ira contribution order suggests prioritizing two other types of accounts.

First, consider prioritizing hsa vs 401k after employer match. A Health Savings Account (HSA) is often referred to as the ultimate retirement tool because of its triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. In 2026, as healthcare costs continue to rise, the HSA acts as a powerful hedge against one of retirement's biggest expenses. If you don't use the funds for healthcare, after age 65, you can withdraw the money for any purpose, paying only standard income tax—essentially turning it into a traditional 401k with better features.

Second, look at the benefits of investing in roth ira vs 401k after employer match. A Roth IRA offers nuances that a standard 401k does not. While you don't get an upfront tax break, your money grows tax-free, and more importantly, your withdrawals in retirement are tax-free. This provides a valuable hedge against future tax rate increases. Furthermore, Roth IRAs do not have Required Minimum Distributions (RMDs) during the owner's lifetime, allowing for much greater control over your asset location strategy and tax bracket in your golden years.

Step 3: Circling Back to Max Out Your 401k

If you have fulfilled your employer match, cleared your high-interest debt, and maxed out your HSA and Roth IRA, it is time to return to the 401k. This is the stage where you aim for the 2026 individual 401k limit of $24,500.

The primary reason to return to the 401k rather than moving to a taxable brokerage account is the benefit of tax-deferred growth. In a 401k, you can trade assets, rebalance your portfolio, and collect dividends without triggering a capital gains tax event every year. This creates a compounding effect that a taxable account cannot match.

When comparing maxing out 401k vs taxable brokerage accounts, also consider legal protections. 401k assets are generally protected from creditors under ERISA (Employee Retirement Income Security Act), providing a layer of security that standard brokerage accounts lack.

| Contribution Type | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| 401(k) Individual | $23,500 | $24,500 | +$1,000 |

| Catch-up (Age 50+) | $7,500 | $7,500 | $0 |

| Super Catch-up (Age 60-63) | $10,000 | $11,250 | +$1,250 |

| HSA (Individual) | $4,300 | $4,400* | Projected |

Special Considerations for 2026: High Earners and Late Starters

The 401k contribution strategy for high earners in 2026 involves navigating several new administrative hurdles created by the SECURE 2.0 Act. One of the most significant changes involves the FICA wage threshold. If your prior-year wages exceeded $150,000, the IRS now mandates that any catch-up contributions you make must be made into a Roth account. This means you will not get an immediate tax deduction on those extra funds, though they will grow and be withdrawn tax-free later.

For those in their 60s, 2026 introduces the "Super Catch-up" window. For participants aged 60, 61, 62, or 63, the catch-up limit increases to $11,250 (or 150% of the standard catch-up limit). This is a massive opportunity for late starters to aggressively bridge any gaps in their retirement readiness.

For high earners whose income exceeds the limits for direct Roth IRA contributions, the Backdoor Roth conversion remains a potent strategy. By contributing to a non-deductible Traditional IRA and quickly converting it to a Roth, you can still access the tax-free benefits of a Roth account even if your income is well into the six or seven figures.

Pro-Tip: Review your 401k plan's Summary Plan Description (SPD). Some plans allow for "After-Tax" contributions above the $24,500 limit, which can then be converted to a Roth 401k or Roth IRA via a "Mega Backdoor Roth" strategy. This can potentially allow you to save up to $72,000 total in tax-advantaged accounts for 2026.

FAQ

Should I contribute more than my employer match to my 401k?

Yes, you should typically aim for a total savings rate of 15%, but the order of operations matters. Once you receive the full employer match, it is often more tax-efficient to prioritize a Health Savings Account (HSA) or a Roth IRA before returning to the 401k to reach the annual limit. This strategy maximizes tax-free growth and gives you more flexibility with your money.

Is it better to contribute to a 401k or a Roth IRA?

It depends on your current tax bracket compared to your expected bracket in retirement. A Traditional 401k provides an immediate tax deduction, which is great for high earners. A Roth IRA uses after-tax dollars but allows for tax-free withdrawals and has no required minimum distributions. Most experts suggest capturing the 401k match first, then filling the Roth IRA for its unique flexibility and tax-free benefits.

Should I contribute to my 401k if I have high-interest debt?

You should contribute just enough to get the full employer match because the 100% return is usually higher than any debt interest rate. However, once the match is secured, you should stop contributing to retirement and focus every extra dollar on paying off high-interest debt like credit cards. Only after that debt is gone should you increase your retirement contributions.

What is the best 401k contribution strategy for beginners?

The best strategy for beginners is to start by contributing enough to get the full company match immediately. From there, set up an automatic increase (often called auto-escalation) to raise your contribution by 1% each year. This helps you move toward the 15% goal gradually without feeling a major hit to your take-home pay.

How do I determine my 401k contribution limit for the year?

The individual contribution limit for 2026 is $24,500. If you are age 50 or older, you can add a catch-up contribution of $7,500. If you are specifically between ages 60 and 63, you can take advantage of the Super Catch-up limit of $11,250. Note that these limits apply to your own contributions; your employer’s matching funds do not count toward this individual limit but fall under a larger $72,000 total limit.